The automotive industry has reinvented itself before. Lean manufacturing reshaped cost structures. Electrification redefined propulsion. Software-defined vehicles are transforming the product itself.

A more consequential shift is now underway: the rise of agentic AI, autonomous systems capable of reasoning, planning, and executing multi-step workflows across enterprise boundaries.

Unlike traditional AI models that optimize single tasks, agentic systems orchestrate outcomes. They connect data, make bounded decisions, trigger downstream actions, and adapt based on feedback. In an industry defined by operational complexity and narrow margins, that distinction is significant.

The strategic question facing automotive leaders is not whether AI will transform the industry. It already is. The real question is whether organizations are prepared to operationalize AI agents at scale while maintaining governance and control.

Why automotive is structurally primed for Agentic AI

Few industries combine the same degree of workflow complexity as automotive. A single vehicle transaction can involve customer relationship systems, dealer management platforms, OEM allocation engines, trade-in valuation tools, captive finance underwriting systems, compliance modules, logistics providers, and warranty databases. Historically, humans have connected these systems through email, spreadsheets, and manual approvals.

Agentic AI replaces manual coordination with structured orchestration.

At the same time, the data foundation has never been stronger. Connected vehicles continuously generate telemetry. Enterprise systems contain decades of structured production, service, and finance data. The constraint is no longer information scarcity. It is workflow integration.

The economic upside is substantial. McKinsey estimates that artificial intelligence could unlock $300–$400 billion in annual value across the automotive sector by 2030¹. Gartner warns that more than 40% of current agentic AI initiatives may be canceled by 2027 due to cost overruns, integration failures, or weak governance².

The opportunity is significant, but execution risk is equally material.

Capital allocation signals a structural shift

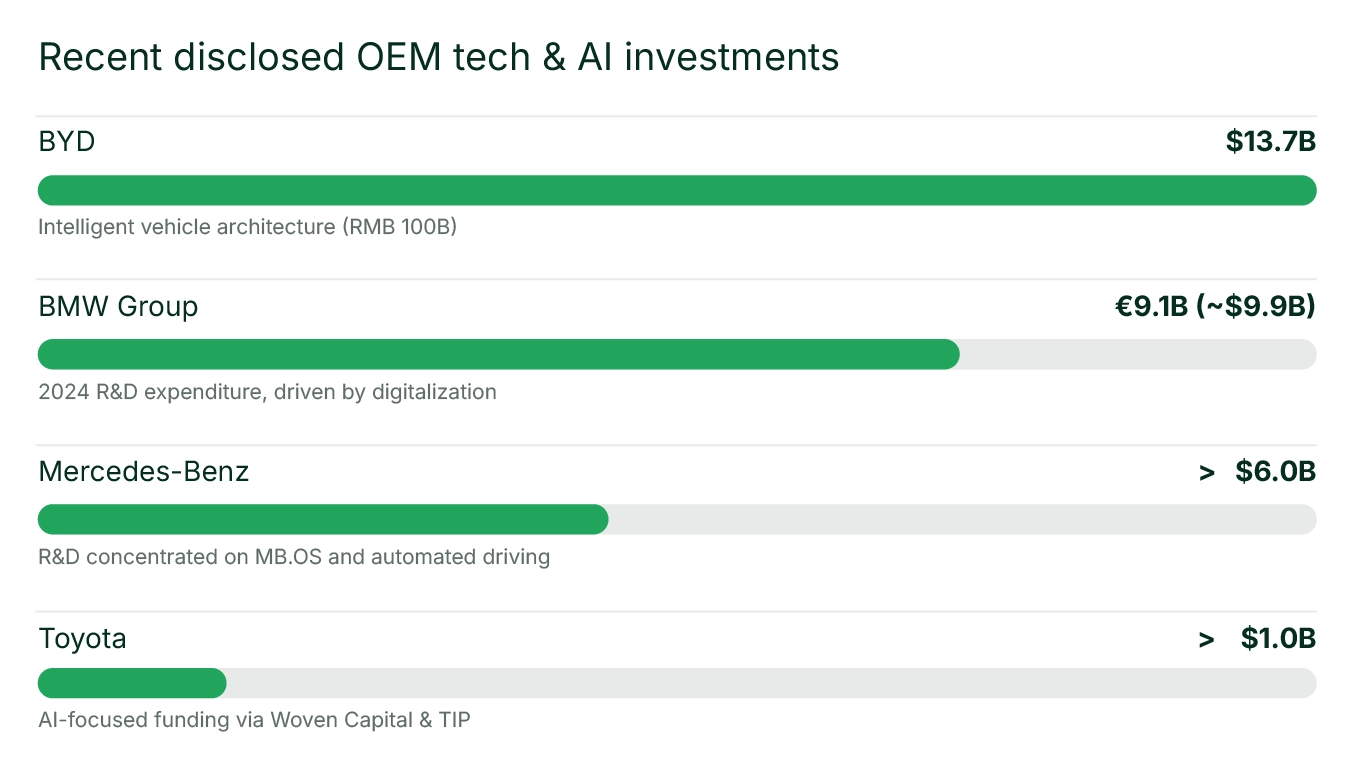

Note: Figures represent distinct programmatic investments or recent annual R&D spend focused heavily on software and AI capabilities. Hyundai also committed KRW 50T (approximately $36B) to future technologies over five years.

Financial disclosures from global OEMs indicate that this transition is structural.

BMW’s R&D expenditure reached €9.1 billion in 2024, representing 6.4% of revenue, largely driven by digitalization and next-generation vehicle architectures³. Mercedes-Benz reported over $6 billion in R&D, concentrated on MB.OS and automated driving systems⁴. Hyundai committed KRW 125 trillion over five years, with more than KRW 50 trillion allocated to future technologies including AI and software-defined vehicles⁵. Toyota’s Woven Capital and Toyota Invention Partners have committed well over $1 billion in combined AI-focused funding⁶. BYD announced a RMB 100 billion investment in intelligent vehicle architecture⁷.

These figures reflect a clear consensus: future enterprise value in automotive will be driven less by mechanical throughput and more by intelligent orchestration.

However, capital deployment alone does not ensure advantage. Volkswagen’s CARIAD software division reported multi-billion-dollar operating losses, illustrating how large-scale digital transformations can erode value when sequencing and governance are misaligned⁸.

The differentiator will not be AI spending. It will be disciplined deployment.

Where Agentic AI is already creating value

Accelerating R&D cycles

Product development in automotive has traditionally been capital-intensive and time-consuming. Generative and agentic AI systems now assist engineers in simulating aerodynamic properties, optimizing materials, and generating software code for infotainment and ADAS systems.

McKinsey research suggests that AI-enabled development can reduce component development timelines by 10% to 20%¹. Academic studies indicate that AI-driven simulation can reduce physical prototyping requirements by as much as 40% to 60% in certain applications, compressing capital cycles.

In a business where new platform launches require billions in upfront investment, even incremental time reductions materially improve capital efficiency.

Reinventing procurement and supply chain

Procurement has historically been reactive. Agentic AI shifts the model toward predictive sourcing.

Intelligent workflow agents can monitor global supplier risk signals, tariff changes, and commodity pricing in real time. McKinsey analysis indicates that AI-enabled supply chain orchestration can reduce inventory and logistics costs by more than 20% in certain deployments⁹. Deloitte identifies a group of “Digital Masters” allocating up to 20% of procurement budgets to advanced technologies, nearly double historical averages¹⁰.

In an industry frequently disrupted by geopolitical shocks and semiconductor shortages, predictive orchestration becomes a strategic buffer.

Transforming retail and dealership economics

Retail automotive remains one of the least digitized segments of the value chain and one of the most margin-sensitive.

Surveys indicate that over 60% of drivers want AI assistance in vehicle selection, and roughly 70% would use AI agents for real-time vehicle diagnostics¹¹. Dealership adoption is accelerating, with 68% reporting positive operational impact from AI initiatives¹¹.

AI-driven pricing and inventory management tools have demonstrated improvements in gross profit per vehicle and service utilization rates. In oversupplied markets, dynamic pricing and predictive demand modeling serve not merely as efficiency tools but as risk mitigation mechanisms.

The dealership of the future will augment human advisors with persistent digital concierges capable of managing follow-ups, financing coordination, and lifecycle engagement.

Reimagining warranty and after-sales

Warranty expenses typically range from 2% to 5% of product revenues. Claims processing has traditionally been manual and prone to leakage.

Agentic systems can cross-reference repair claims against diagnostic patterns, flag anomalies, and automate adjudication of standard cases. Gartner predicts that by 2029, agentic AI could autonomously resolve 80% of common customer service issues, reducing operational costs by approximately 30%².

Combined with predictive maintenance from connected vehicle telemetry, warranty shifts from reactive cost center to predictive margin protection engine.

Captive finance: a high-leverage opportunity

Captive finance arms generate a disproportionate share of OEM profitability.

Machine learning underwriting platforms have demonstrated measurable reductions in default losses. One implementation for a major U.S. captive lender resulted in a 23% decrease in default rates among sub-720 FICO borrowers¹². McKinsey estimates that generative and agentic AI could reduce cost-to-income ratios in auto finance by five to eight percentage points¹.

Beyond efficiency, improved underwriting expands safe credit access and strengthens long-term customer loyalty.

The underestimated risk: human–AI orchestration

Scaling agentic AI introduces organizational complexity.

A nationwide occupational audit conducted by Stanford researchers found that 41% of AI task mappings fall into an “Automation Red Light Zone,” where current systems lack sufficient contextual reasoning for safe autonomous operation¹³.

In automotive, this has material implications. Engineers and underwriters may accept AI assistance while resisting full autonomy in safety-critical or regulatory-sensitive domains.

The implication is not slower adoption, but role redesign. The workforce will shift from manual execution toward supervision, validation, and governance of digital labor. Organizations that redesign operating models, rather than layering automation onto legacy structures, will realize greater advantage.

Moving from hype to maturity

Most automotive organizations remain in early stages of agentic adoption, deploying isolated bots or narrow pilot programs. Greater value emerges when agents orchestrate cross-domain workflows.

Industry maturity typically progresses through:

- Task automation

- Simple orchestration within a single function

- Cross-domain workflows

- Multi-agent collaboration across ecosystems

- Governed, autonomous enterprise-wide systems

Premature acceleration without foundational data harmonization and governance controls introduces risk.

The strategic inflection point

The automotive industry is transitioning from mechanical scale to software monetization and now to intelligent orchestration.

The next decade’s leaders will not necessarily be those who invest the most in AI. They will be those who integrate AI into core workflows, govern it rigorously, redesign roles around digital labor, and build interoperable agent ecosystems.

Agentic AI represents not merely a digital tool, but a shift in operating model design.

The question is not whether AI agents will become embedded across the automotive value chain, but how effectively leaders will shape and govern that transformation.

References

- McKinsey & Company, “The Road to Artificial Intelligence in Mobility,” 2025.

- Gartner, “Predicts 2025: AI Agents Will Transform Enterprise Operations,” 2024.

- BMW Group, Annual Report 2024.

- Mercedes-Benz Group AG, Annual Report 2024.

- Hyundai Motor Group investment disclosures, 2025.

- Toyota Motor Corporation; Woven Capital Fund announcements.

- BYD Company intelligence investment disclosures.

- Volkswagen Group / CARIAD financial reporting.

- McKinsey supply chain AI analysis.

- Deloitte Global CPO Survey, 2024.

- CDK Global automotive AI adoption survey, 2025.

- ZestFinance case study (Big Three captive lender).

- Stanford University occupational AI capability audit, 2024.

FAQs:

1. What is agentic AI?

Agentic AI refers to autonomous AI systems that can plan, reason, and execute multi-step workflows across enterprise systems while operating within governance boundaries.

2. Why is automotive suited for agentic AI?

Automotive organizations operate complex workflows across manufacturing, supply chains, dealerships, finance, and after-sales services, making them ideal environments for AI agents that orchestrate multi-system processes.

3. What is an agentic enterprise?

An agentic enterprise deploys networks of AI agents to automate decision workflows, coordinate systems, and continuously optimize operations.

4. How can automotive companies deploy agentic AI safely?

Successful deployment requires strong data governance, AI security, human oversight, and well-defined operational guardrails.